China Escalates Crypto Ban

Ethereum drops more than Bitcoin as China escalates crypto ban, ETH/BTC at 3-week low

The second-largest cryptocurrency falls 13.30% versus Bitcoin’s 9.38% decline as China’s move scares investors away.

Image courtesy of CoinTelegraph

SEPTEMBER 24, 2021

SEPTEMBER 24, 2021

The price of Ethereum’s native token Ether (ETH) crept lower Friday after China extended its crackdown on cryptocurrencies by deeming their transactions to be “illegal.”

“Financial institutions and non-bank payment institutions cannot offer services to activities and operations related to virtual currencies,” the People’s Bank of China said in a statement on its website Friday, adding that online crypto services to Chinese residents offered by offshore exchanges are also “illegal financial activities.”

Bids for the ETH/USD pair dropped by up to 13.30% to $2,735 in response. At its week-to-date (WTD) high, traders paid as much as $3,346 for a single Ether token but the price fell to as low as $2,651 after a tumult in China’s heavily indebted property sector hit crypto markets.

ETH/USD daily price chart. Source: TradingView.com (Click image for larger view)

As a result, Bitcoin (BTC), the world’s leading cryptocurrency, also fell from its WTD high of $47,358 to as low as $2,651. Meanwhile, its prices fell by 9.38% on Friday—a massive intraday decline but lower than Ether’s drop in the same period.

So it appears that traders decided to dump the digital assets that posted better long-term profits than Bitcoin. For instance, even after the latest declines, ETH/USD’s year-to-date (YTD) gains came out to be above 280%. In contrast, Bitcoin’s YTD profits were a little over 40%.

ETH/BTC falls to multi-week lows

Ether also underperformed directly against Bitcoin, with the ETH/BTC pair falling to 0.066 BTC for the first time in more than three weeks. At its yearly high, the pair traded at 0.079 BTC.

ETH/BTC daily price chart. Source: TradingView.com (Click image for larger view)

Nonetheless, Ethereum charts suggest that Ether could grow stronger against Bitcoin in the coming sessions. This is due mainly to a Bull Flag formation in ETH/BTC market, a bullish continuation pattern that surfaces when prices consolidate lower/sideways (FLAG) following a strong uptrend (FLAGPOLE).

A Bull Flag typically sets its profit targets at length equal to the Flagpole’s size if the price breaks above its channel’s upper trendline. That said, ETH/BTC may undergo a bullish breakout to eye its previous local high of 0.0824 BTC.

Bullish fundamentals persist

Meanwhile, the Ethereum token also expects to surge overall because of its growth in the emerging decentralized finance (DeFi) sector. As Cointelegraph reported earlier, the total value locked (TVL) across the decentralized applications (DApp) industry reached $142 billion in August 2021, out of which 68% was concentrated on the Ethereum network.

Related: Ethereum forming a double top? ETH price loses 12.5% amid Evergrande contagion fears

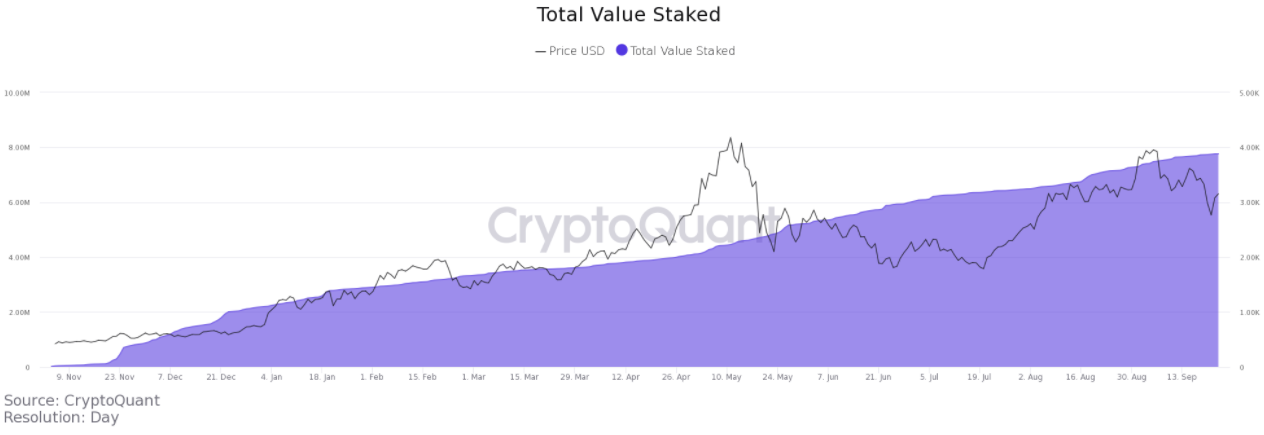

That ensures more demand for Ether tokens for its ability to power smart contracts that back DApps. On the other hand, its active supply across the board anticipates declines as holders continue to lock their ETH holdings into Ethereum’s proof-of-stake smart contract.

The total value staked into the Ethereum PoS smart contract has jumped from 11,616 ETH to 7.76 million ETH in nine months. Source: CryptoQuant (Click image for larger view)

More supply is expected to go out of circulation as the Ethereum network continues to burn a portion of its daily 13,000 ETH issuance following its Aug. 5 London hard fork upgrade. According to WatchTheBurn, the network has burned 358,616 ETH worth over $1 billion.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Advertisement

Original article posted on the CoinTelegraph.com site, by Yashu Gola.

Article re-posted on Markethive by Jeffrey Sloe